Licensed 280E/471(c) representation you plug into your practice.

You build the cannabis tax work. You just can’t sign or defend it. I’m the Enrolled Agent who does, working as your back office, so you keep the client while their returns get signed, disclosed, and represented. I never take your client.

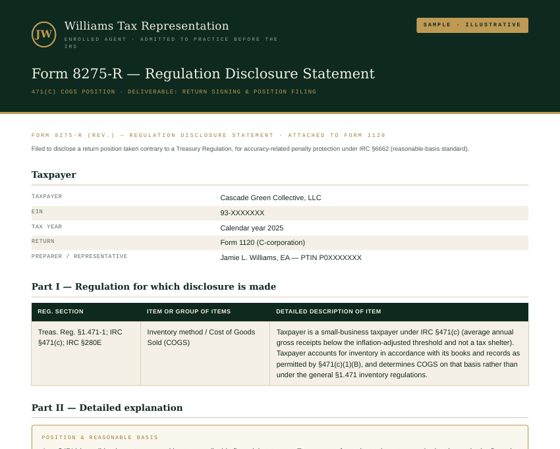

Positions you can’t sign

Aggressive 280E/471(c) work needs a licensed EA or CPA to sign and represent. Without one, the return sits exposed.

A credential on the POA

An Enrolled Agent, admitted to practice before the IRS, signs the return and stands in front of the IRS when a notice lands.

The work, not a promise

Every engagement produces a defined, signed deliverable, disclosed and defensible. No clients named, no reviews. The outcome is the proof.

One licensed engagement.

Start with a single client: sign and file one 471(c)-disclosed return, or take one exam or collections case, delivered end to end and tracked in your portal.

One consult, one engagement, one proof point. Scale to your whole cannabis book once it works.

Enrolled Agent admitted to practice before the IRS. General information, not legal or tax advice. Representation begins only under a signed engagement.