Hand off your cannabis clients' IRS problems. Get them back signed, defended, resolved.

A complete 280E/471(c) representation service you plug into your practice. You keep the client and the books; I deliver the licensed work product under my Enrolled Agent signature.

Admitted to practice before the IRS in all 50 states. Exam defense · Appeals · Collections · Form 8300.

Under §280E, a compliant cannabis operator is taxed on gross profit, not net.

The full-service cannabis firms will take your whole client. I won't.

Refer a client to a full-service cannabis CPA firm and you can lose them, because those firms sell fractional-CFO services too. I work the other way: back-office representation only. I sign and defend the work, you keep the client, the books, and the relationship. Your clients never need to know my name.

Strategy & the books

- The client relationship and monthly financials

- Cost accounting and the 471(c) methodology

- Cash-flow, planning, and lender packages

- The advisory seat at the table

The representation lane

- Return signing & filing, with a documented disclosure gate

- Power of Attorney (Form 2848) before any IRS contact

- Exam defense — IDR responses & the COGS substantiation file

- Appeals, collections, liens, levies, and penalty relief

Back-office representation, in writing.

The engagement is built so you never have to wonder where your client stands. Five things it puts on paper, and the result.

I stay behind the scenes

I work as your back office. The client stays yours; your clients never need to know my name.

I never take your client

A written non-solicitation: I don't market to, pitch, or accept your clients for any service. In the agreement, not just a promise.

Who signs, who represents

A per-client engagement letter defining exactly what I sign, what I represent, and the disclosure gate for every position.

Your data stays protected

Written §7216 consent before any taxpayer information moves. Nothing touches a third party or AI tool without it.

No ambiguous lanes

The credential on the return and the Power of Attorney is defined up front, so responsibility is never a grey area.

You grow without losing ground

You take on cannabis work you couldn't complete before, keep every client, and put a licensed credential behind the risk.

What I take off your desk.

Priced per engagement or on a monthly review. Bring me in on one client or your whole cannabis book.

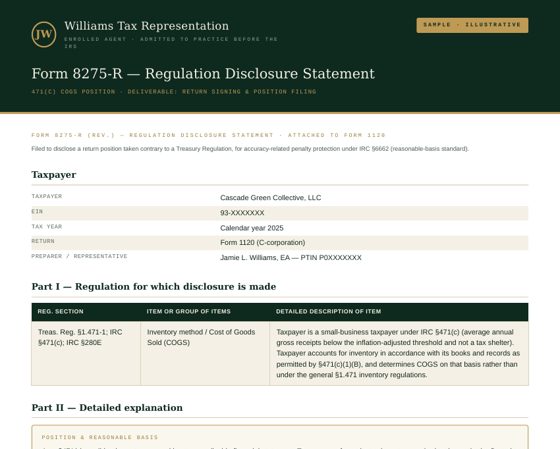

Return signing & position filing

Business and personal returns for cannabis and high-earner clients, with a written COGS / 471(c) risk policy and a mandatory Form 8275-R disclosure gate for penalty protection.

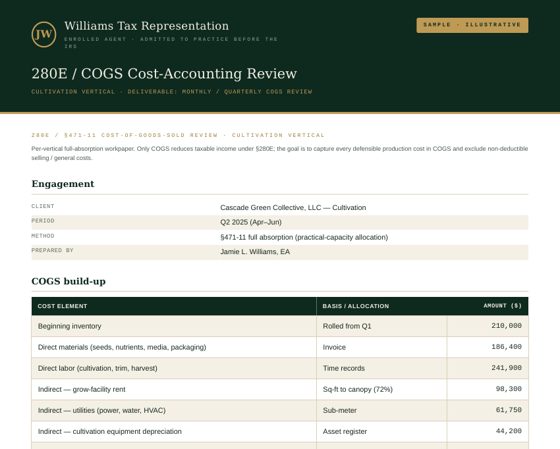

280E / COGS cost-accounting review

Per-vertical full-absorption workpapers — cultivation, manufacturing, retail — recomputed monthly or quarterly so every defensible dollar lands in COGS and nothing that shouldn't.

Rescheduling transition planning

Medical-vs-adult-use license analysis, amended-return and retrospective-relief evaluation as IRS guidance lands. The 2026 window changes what your clients owe.

Audit defense & Appeals

IDR responses, record reconstruction from bank / POS / METRC, the RAR review, and the protest to the IRS Independent Office of Appeals. Per engagement.

Collections resolution

Liens and levies, installment agreements, Currently Not Collectible, Offers in Compromise, and penalty abatement — the full resolution toolkit.

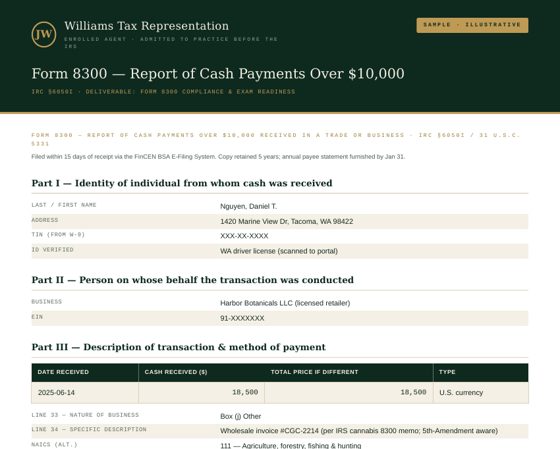

Form 8300 compliance & exam readiness

Cash-reporting cleanup for unbanked operators, the SOP so it stops recurring, and defense when the $10k-cash penalties surface.

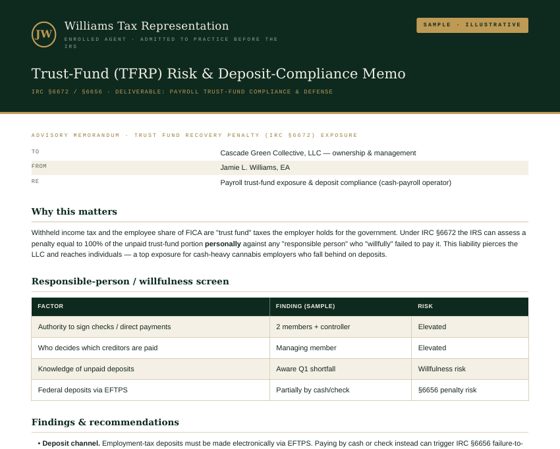

Payroll trust-fund & TFRP defense

Deposit compliance for cash-payroll operators and defense against the Trust Fund Recovery Penalty — the one that reaches owners personally.

The work product, not a promise.

Every engagement produces a defined, signed deliverable that lands in your portal. No client logos. No testimonials. The outcome is the proof, so here is exactly what the work looks like.

Samples · illustrative data · your clients' work stays confidential

A defined delivery pipeline. Every engagement runs the same seven phases.

You always know where a client's work stands, captured through closed, tracked in your secure portal from first upload to final filing.

Info

Client and matter captured; the exposure is identified.

Scope

Engagement confirmed; position and disclosure path set.

Assets

Records collected: bank, POS, METRC, payroll.

Draft

Deliverable built; workpapers and disclosures prepared.

Delivery

Signed, filed, or submitted to the IRS for your client.

QA

Reviewed against Harborside and current statute; report issued.

Exit

Outcome validated, next state logged, support window open.

Nothing is "done" until the outcome is validated. Each phase has a defined finish line, so work never stalls, disappears into email, or ends without a next step.

The rules are moving. This is the moment to get positions and representation right.

Executive order

Directs DOJ to reschedule medical marijuana "expeditiously."

Medical → Schedule III

State medical-licensed operators leave §280E for tax year 2026. Retrospective relief under review.

Broader hearing

DEA hearing on rescheduling all marijuana concludes. Outcome pending; challenges expected.

Adult-use stays stuck

Recreational and unlicensed activity remain Schedule I — §280E still applies. Most operators still need a defense.

A clean hand-off, not a hand-over of your client.

Scope call

We map which of your clients carry exposure and where a licensed representative is needed.

Engagement & POA

A defined engagement letter per client, position-disclosure sign-off, and Form 2848 on file.

I represent

Signing, exam defense, appeals, or collections — I stand in front of the IRS; you keep the books.

You stay informed

Documented positions, clear updates, and a defense file your client can rely on if the notice comes.

A credential you can put on a Power of Attorney.

An Enrolled Agent is federally licensed to represent any taxpayer, for any tax matter, before every office of the IRS. That is the authority a 471(c) position needs standing behind it — and the authority your clients are asking you for.

Every aggressive position is disclosed, not hidden. Every year is checked against Harborside and the current statute before a client is told it's closed. Nothing goes to the IRS without verification.

Admitted before the IRS

Represent, sign, and file in all 50 states — exam, appeals, and collections.

Disclosure-gated method

Form 8275 / 8275-R on aggressive positions — penalty protection built in, not bolted on.

Cannabis-native

Per-vertical COGS, cash-heavy 8300 exposure, and trust-fund risk — the traps generalists miss.

Everything runs inside one secure portal.

You and your clients work in a private, encrypted portal — intake, documents, deliverables, and status in one place. PII stays access-controlled and audit-ready from the first upload to the final filing.

- Encrypted client portal — one login, full history, nothing in email.

- PII access-controlled from intake to delivery.

- Every deliverable tracked, versioned, and logged.

- AI-assisted where it speeds delivery, never without §7216 consent, never outside the portal.

Priced against what you'd lose, not what you'd pay a preparer.

One defined engagement, one flat price. Sending the client to a full-service firm risks losing them; this keeps them yours. Every engagement starts with a paid Risk Review, credited toward your first tier.

Sign & File

- 471(c)-disclosed return, signed & filed

- Form 8275-R disclosure + COGS workpaper

- Power of Attorney (Form 2848)

- First IRS notice response

Sign & Defend

- Everything in Sign & File, for that client

- Representation on notices & exam first-response

- A named EA on the client all year

Standing Representation

- EA-of-record across your cannabis clients

- Ongoing signing + first-line defense

- Stepped by book size (≤5 / ≤10 / 10+)

Prices cover defined scope. A matter that escalates into a full exam, Appeals, or collections is scoped separately, so a fixed fee never rides on open-ended risk. This is general information, not legal or tax advice; representation begins only under a signed engagement.

How the partnership works.

Do you replace my role with the client?+

Whose PTIN and signature go on the return?+

How do you handle aggressive 471(c) positions?+

Can you take a client already in an audit or in collections?+

What does the rescheduling change for my clients?+

How fast do you respond?+

Give your cannabis book a name on the Power of Attorney.

A 30-minute partnership consult: which of your clients carry exposure, and where a licensed representative earns its keep.